created by Gpt

Global Factoring Market 2025: €4 Trillion. What risks come with the growth?

The global factoring market surpassed €4 trillion in 2025. Europe still dominates with nearly two-thirds of all transactions, while China solidifies its position as the largest single-country market. Where is the industry heading — and what risks come with the growth?

Global Factoring Market 2025: €4 Trillion in Turnover

Europe holds 65.8% of the market, China continues scaling up its volumes, and global trade is shifting further toward open account terms. Where are the growth drivers, and where are the turbulence zones?

Factoring enables companies to accelerate payment for deferred-payment supplies: the supplier assigns the monetary claim against the buyer to the factor and receives financing before the payment due date. This article examines the structure of the global factoring market, its total volume according to FCI data, the leading regions, and the key factors that will influence market growth in the coming years.

What Is Factoring and Why Does It Matter for Global Trade

Definition of Factoring

Factoring is financing against the assignment of a monetary claim. In simple terms, you sell the right to collect payment from your buyer to a factoring company (the factor). Modern trade operates almost exclusively with deferred payment terms. A supplier ships goods but only receives payment after 30 to 120 days. Factoring bridges this cash flow gap. The funds transferred by the factor to the supplier go directly into working capital. The company can pay salaries, purchase raw materials, and grow without waiting for the buyer's payment.

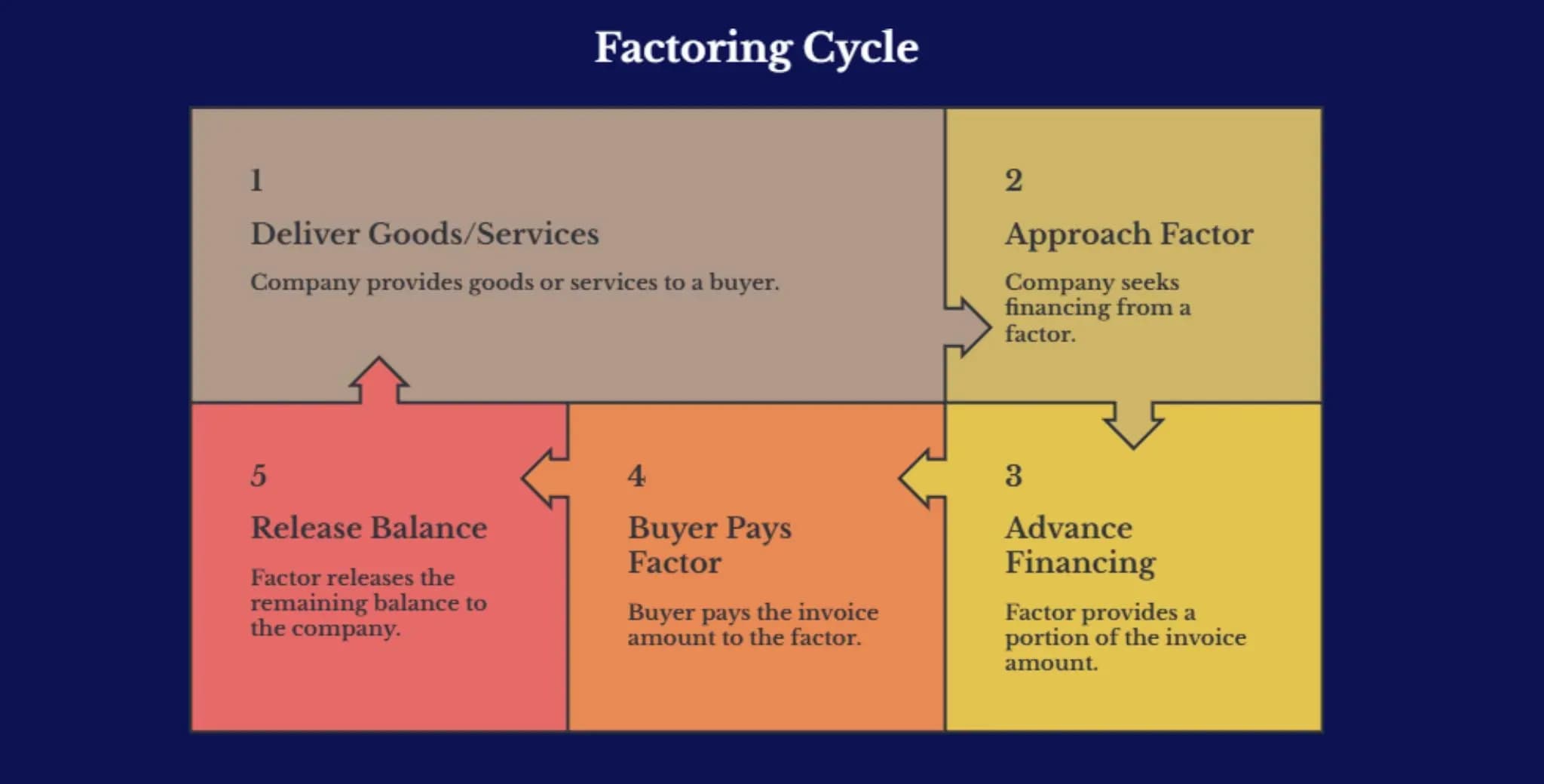

How Factoring Works

1. The company delivers goods or services.

2. It then approaches a factor to obtain financing against the assignment of the monetary claim.

3. The factor advances the client a substantial portion of the invoice amount.

4. The buyer transfers the payment to the factor when the invoice matures.

5. The factor releases the remaining balance, minus its service fee.

created by Napkin

Global Factoring Market Volume and Dynamics

According to FCI (Factors Chain International), the market stood at €3,895 billion in 2024. That year was stable, with the market consolidating after the active post-pandemic recovery period. The 2025 growth demonstrates that factoring remains resilient even amid global uncertainty. Geopolitical tensions and shifts in trade flows have not broken the mechanism. Nearly 90% of international trade today is conducted on open account terms — i.e., with deferred payment, without letters of credit or advance payments. Factoring is one of the key financial instruments supporting this trade format. Domestic factoring (both parties in the same country) still accounts for the majority of the market, but international factoring is growing at a faster pace.

Structure of the Global Factoring Market

Any factoring transaction involves three core parties: the supplier (your company), the buyer (your client), and the factor (a financial institution or bank). Insurers may also participate in the chain to cover the buyer's default risk. When industry professionals refer to factoring market turnover, they mean the aggregate value of all assigned invoices over a given period. According to FCI data, this figure reached €4 trillion in 2025.

Do not confuse turnover with factors' revenue. Turnover represents the total value of financed deliveries, whereas revenue consists of the fees and interest earned by the factor. Factoring is a subset of the broader trade finance market and is closely related to supply chain finance. The distinction lies in who initiates the transaction. In classical factoring, the supplier is the initiator. In reverse factoring (supply chain finance), a large buyer initiates the process to help its suppliers receive faster payments.

Global Factoring Market Growth Forecasts

Analytical firms expect moderate growth in the global factoring market over the coming years. According to Mordor Intelligence estimates, the compound annual growth rate (CAGR) may reach approximately 6% between 2026 and 2031. Digitalization and electronic invoicing reduce operational costs, making factoring more accessible to small businesses and smaller exporters. Small and medium-sized enterprises often cannot obtain bank loans, yet their receivables are reliable. Factoring solves this problem. Emerging markets demonstrate higher growth dynamics, but their share of global turnover remains limited due to weak infrastructure. The primary downside risk is a global recession accompanied by rising default rates. Factoring is not immune to credit crises.

Key Regions of the Global Factoring Market

The global factoring market varies significantly by region depending on economic conditions, payment culture, and legal frameworks.

Europe is the largest regional factoring market.

According to FCI, Europe accounted for approximately 65.8% of global factoring turnover in 2025. Banks and institutional infrastructure play a major role here. Factoring is often embedded into business settlement and cash management services. Electronic document flow and credit insurance are well developed in Europe, reducing risks and accelerating transactions. The leading countries in the region — France, Germany, the United Kingdom, Italy, and Spain — account for the majority of European factoring volume.

Asia-Pacific Region

The Asia-Pacific region is the second largest factoring market. According to FCI, its share reached 26.4% of global turnover in 2025. China is the largest single-country factoring market. In 2024, factoring turnover in China reached €679 billion. India, Singapore, Japan, and Hong Kong are growing rapidly. The expansion of supply chains and international trade continues to support demand.

North and South America

This region demonstrated the strongest growth in 2025 — up 20% to €326 billion. North America grew by 35.1%, primarily driven by the United States. The U.S. market is undergoing active digitalization, with rising demand for working capital financing. South and Central America added 8.2%, reaching €165 billion. Brazil grew by 22.2%.

Africa and the Middle East

Africa and the Middle East currently account for a modest share of global factoring. However, the growth potential is substantial. Regulatory development and trade expansion are laying the groundwork for growth. Several countries are introducing factoring-specific legislation. Key barriers include weak legal infrastructure, a lack of credit data, and high default risk. The cost of funding in the region is higher than in Europe.

Major Types of Factoring in the Global Economy

Depending on the countries of the parties involved, the risk allocation, and the buyer's role in the transaction, factoring can be classified into several key types.

Domestic and International Factoring

In domestic factoring, the supplier and buyer are located in the same country. This is the most common type.International factoring is used in export-import transactions and often employs a two-factor model: an export factor and an import factor.

Recourse and Non-Recourse Factoring

Under recourse factoring, the default risk remains partially with the supplier. If the buyer fails to pay, the supplier reimburses the factor. Non-recourse factoring means the factor assumes the debtor's default risk within the terms of the agreement. This is more expensive but safer for the supplier. Non-recourse factoring typically requires credit insurance and a thorough assessment of the debtor.

Reverse Factoring / Supply Chain Finance

Reverse factoring is initiated by a large buyer. The buyer arranges with a factor to pay its suppliers' invoices early. Suppliers receive funds sooner, while the buyer retains its deferred payment terms. The factor assesses the buyer's risk rather than (or in addition to) the supplier's.This instrument is critical for managing large supply chains.

Export and Import Factoring

For an exporter, factoring provides immediate payment after shipment. There is no need to wait 60–90 days for payment from a foreign buyer. Factoring is particularly useful when an export contract includes deferred payment terms. It is simpler and faster than a letter of credit.In international factoring, documentation, jurisdiction, currency, and the buyer's payment discipline are all critical. Errors on an invoice can block financing.

More on the topic

The expansion of private lending in trade finance: chance or gap?

Explore how private credit funds are transforming global trade finance, closing liquidity gaps while creating new risks. Based on IMF data, Edenex expertise, and 2025 market lessons.

Factoring Has Stopped Being a Paper-Based Game?

From tokenized Treasuries to direct invoice financing. Real use cases, active protocols, regulatory moves, and the gap between on-chain efficiency and legal reality.

Drivers of Global Factoring Market Growth

The growth of deferred-payment trade is the primary structural driver. The longer the deferral period, the greater the demand for factoring. Companies face acute working capital needs. Banks often reject small businesses, while factoring remains accessible. The high cost of traditional lending makes factoring more attractive. Loan rates are rising, whereas factoring is tied to specific deliveries. Digitalization of document flow reduces transaction costs. Electronic invoices accelerate verification and funding. The development of scoring models and digital platforms enables faster risk assessment. Data on payment discipline is becoming increasingly available. The integration of factoring with credit insurance expands the range of possibilities. Factors can assume larger risks without compromising their position. Emerging economies are improving their factoring legislation, attracting international players. The restructuring of global supply chains creates new goods flows. Every new deferred-payment contract represents a potential factoring transaction.

Global Factoring Market Trends

The market is shifting from paper documents to digital platforms. Factoring without electronic invoices is becoming the exception.

Supply chain finance is growing faster than classical factoring. Large companies are embedding financing into their supplier management processes.

Embedded finance is penetrating the factoring space. E-commerce platforms offer financing as an integrated service.

Data and debtor scoring are replacing traditional underwriting. Factors are increasingly assessing thousands of small debtors automatically.

Emerging regions are showing growing interest in factoring, although mass explosive growth has not yet materialized.

Compliance, KYC/AML requirements, and transaction transparency are becoming stricter. Factors are allocating increasing resources to due diligence.

Risks and Limitations of the Global Factoring Market

Despite the growing popularity of factoring in international trade, the instrument carries a set of risks that extend well beyond ordinary accounts receivable.

Credit risk of the debtor— the primary risk in factoring. If the buyer defaults, the factor or the supplier suffers a loss.

Concentration risk with major buyers is dangerous. The loss of a single large debtor can destabilize an entire portfolio.

Invoice fraud is a persistent challenge. Fictitious deliveries, double financing, and forged documents are regular occurrences.

Legal differences between jurisdictions complicate international factoring. The assignment of receivables is not recognized uniformly across all legal systems.

Cross-border debt collection is complex and expensive. Even if the factor wins a court judgment, recovering funds from a foreign debtor remains difficult.

Currency risk affects international transactions. The factor must hedge its exposure or operate only in a single currency.

Rising funding costs compress factors' margins. When central banks raise interest rates, factoring becomes more expensive.

Document and data quality is critical. Any error in an invoice can render it ineligible for financing.

Compliance risks are increasing due to sanctions and anti-money laundering regulations. The factor must screen the supplier, the buyer, and their ultimate beneficial owners.

What the Global Factoring Market Means for Businesses

Factoring solves a key business challenge — the time gap between goods shipment and payment receipt — and offers distinct advantages depending on the company's role in the supply chain.

For suppliers — accelerating cash inflow from deliveries. No need to wait 60–90 days; funds can be received as early as the next day.

For exporters— reducing the cash flow gap and obtaining protection against foreign buyer default. This is especially important when supplying to countries with weak payment discipline.

For buyers — retaining convenient deferred payment terms while the supplier has already received payment from the factor.

For large companies— a supply chain management tool. You can help key suppliers obtain financing, thereby ensuring production stability.

Outlook for the Global Factoring Market

The market remains resilient because it is tied to real trade. As long as businesses sell goods with deferred payment, factoring will be needed. Europe will retain its leadership, but emerging markets will grow faster. China has already become the largest national factoring market, with India following. Digitalization will continue lowering operational barriers. The simpler and faster it is to confirm a delivery, the cheaper and more accessible factoring becomes. Demand from exporters will sustain the market under any economic conditions. When businesses need liquidity, factoring is always relevant. Regulation and legal infrastructure will remain key conditions for growth. Countries with modern factoring legislation will attract capital and develop more rapidly. The market is evolving not only through increased trade volumes. Digitalization and new financing models are creating additional opportunities.

FAQ

What is the global factoring market?

It comprises all transactions in which companies sell their invoices to financial institutions (factors) to obtain immediate financing. The market includes both domestic and international transactions.

What is the volume of the global factoring market?

According to FCI, global factoring turnover reached €4 trillion in 2025.

Why does Europe hold the largest share of the global factoring market?

Due to its developed banking infrastructure, strong regulatory framework, and high adoption of electronic document flow. In 2025, Europe accounted for 65.8% of global turnover.

How does international factoring differ from domestic factoring?

In international factoring, the seller and buyer are located in different countries. Transactions are more complex due to currency differences, multiple jurisdictions, and cross-border collection. A two-factor model is frequently used.

What is non-recourse factoring?

A type of factoring in which the factor assumes the buyer's default risk. If the buyer does not pay, the supplier is not required to reimburse the factor.

What is reverse factoring?

Financing initiated by the buyer. A large company arranges with a factor to pay its suppliers' invoices early, while the buyer pays the factor at a later date.

How does factoring differ from a bank loan?

A loan is granted against collateral for a fixed term, while factoring is based on the sale of a specific invoice without additional collateral. In factoring, the amount depends on sales volume rather than a predefined credit line.

What are the main risks associated with factoring?

Key risks include buyer default, invoice fraud, legal complexities in cross-border transactions, and currency fluctuations.